by Rahul Choudhary | Jan 15, 2025 | Credit Cards

1865: The Birth of the Concept

The first charge coins were issued, kickstarting modern credit card history. These coins allowed customers to pay at the time of the purchase without cash. They were tremendously popular in the farming industry in Western countries during westward expansion, allowing farmers to wait until after their harvest to pay their bills.

1882–1891: American Express

American Express, originally formed in 1850 to rival the U.S. Postal Service, introduced both money orders and travelers’ checks. Both gained popularity in the late 19th century.

1914: Loyalty

Department stores and oil companies began offering proprietary cards to customers, allowing them to buy goods on credit. These cards, predecessors to modern store cards, were much more about securing customer loyalty than offering purchasing convenience.

1946: Charge-It Card

John Biggins, a banker from Brooklyn, introduced the Charg-It card. The card worked on a local, closed-loop system, with all purchases being routed through Biggins’ bank. The bank paid for the purchase, and the customer paid for it through their account at Biggins’ bank later. Five years later, Franklin’s National Bank offered a similar card.

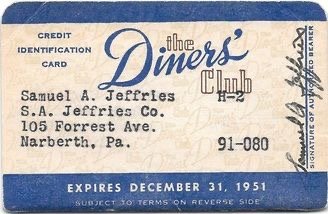

1950: Diners’ Club

The Diners’ Club card was launched after business executive Frank McNamara forgot his wallet during a client lunch. The cardboard card could be used for dining, entertainment, and travel expenses. Though it is considered the first widespread credit card, the Diners’ Club card operated like a charge card—at the end of each month, the bill had to be paid in full. It was also the first card to charge interest payments to its users.

1955: The Term “Credit Card”

The term “credit card” was used in a patent for the first time. This patent ushered in the first gas pump that accepted credit cards.

1958: Travel and Entertainment Card

American Express released their travel and entertainment card geared toward business people who traveled for work. This allowed them to pay for all their business expenses without carrying large sums of cash.

1958: Bank Cards

BankAmericard kickstarted the practice of banks offering cards working on revolving credit when they sent out 60,000 unsolicited cards in the mail in California. The introduction of revolving credit made early iterations into what we know as credit cards today. Customers could carry their remaining monthly balances forward for a fee. By 1966, the card became the first licensed general-purpose credit card.

1959: Plastic Credit Cards

American Express launched the first plastic card made out of PVC, greatly increasing the company’s popularity.

1966: MasterCharge

The Interbank Card Association was formed to stop BankAmericard from monopolizing the industry. The group sought to create the first national credit card system, issuing their card, the MasterCharge (modern-day MasterCard).

1967: ATM

A cash machine was put into use by Barclays Bank in Enfield, United Kingdom, on June 27, 1967, which is recognized as the world’s first ATM.

1968: MasterCard

The Interbank Card Association introduced credit card systems to Mexico, Europe, and Japan, making it the first global card company. This shift also ushered in a new name for the company: MasterCard.

1970: Magnetic Stripe

IBM introduced the magnetic stripe in conjunction with American Airlines and American Express. This form of data transfer prevailed for nearly 50 years but is now being phased out to make way for EMV chips and contactless payment methods.

1973: Advanced Technology

MasterCard and National BankAmericard developed their electronic authorization systems for credit card processing. These systems paved the way for the technologically advanced industry of today.

1976: VISA

BankAmericard expanded outside the United States and changed its name to Visa, now the most widely recognized credit card brand.

1981: Point-of-Sale (POS)

Hawaiian company Verifone developed its first point-of-sale (POS) machine, followed by its popular ZON terminal in 1983. Their machine ushered in widespread use of POS systems.

2014: Digital Cards

Apple introduced its originally unpopular mobile payment digital wallet, Apple Pay. Similar mobile and contactless payment options expanded throughout the 2010s, including Google Pay, Android Pay, Samsung Pay, and others.

2015: Chip Cards

Europay, Mastercard, and Visa partnered to create the EMV chip, which has become standard practice in the credit card processing industry. Chips offer greater security due to their single-use transaction codes.

by Rahul Choudhary | Jan 15, 2025 | Credit Cards

Future for the Credit Card

Debit cards have long competed with credit cards, but they have never pushed credit cards out of the payment space—even during the Great Recession when millennial distrust of credit ran rampant. Knowing debit cards’ biggest failing points is important to understanding why other payment innovations pale when compared to the credit card.

Debit cards rarely give consumers the opportunity to accrue rewards, and they don’t help build a credit score. Debit cards are also at a major disadvantage since credit cards are more secure (and no one agrees more than the author and former fraudster Frank Abagnale). A credit card company will defend you and negotiate on your behalf with the merchant in the event of a fraudulent transaction. Additionally, the funds won’t ever go from your bank account.

The tale changes when a malicious party obtains access to your bank account. If fraud is successfully reimbursed, it may take several months, and while that time the customer is completely cut off from their money.

Debit cards have been present for many years, but a recent development hailed as a competitive payment innovation is the ability to link bank accounts to online activities. You can use your bank to make payments when you pay online. However, where is the consumer advantage? Compared to debit cards, credit cards offer greater protection to users against fraudulent conduct.

Technological Advancements in Credit Cards

Credit cards are changing as a result of the same technology that is propelling fintech innovation. Thanks to this technology, which is built on mobile and digital front ends backed by APIs and SDKs and cloud infrastructure, practically any size business or brand may now offer customized cards.

The same technology that is making plastic cards digital is also revolutionizing rewards programs, taking them beyond basic airline, shop, and cash-back programs. Customers may be able to take advantage of new, helpful perks through new incentive possibilities.

New Opportunities with Credit Cards

As more banks and other financial institutions join the market, they are eager to support co-branded credit cards for smaller companies or groups. Businesses can now provide prizes in cryptocurrency, fractional shares, charitable contributions, payback of student loans, and other areas.

Credit cards are growing into new markets and providing consumers and businesses with a plethora of new opportunities, rather than going extinct. Also, don’t listen to anyone who says otherwise.

by Rahul Choudhary | Jan 15, 2025 | Scams

BANKING SCAMS

Phishing scams are all about tricking you into handing over your personal and banking details to scammers. The emails you receive might look and sound legitimate, but genuine organizations like a bank or a government authority will never expect you to send your personal information by email or online.

Scammers can easily copy the logo or even the entire website of a genuine organization. So don’t just assume an email you receive is legitimate. If the email is asking you to visit a website to ‘update’, ‘validate’ or ‘confirm’ your account information, be skeptical.

Delete Phishing Emails

They can carry viruses that can infect your computer. Do not open any attachments or follow any links in phishing emails.

Fake Fraud Alerts

A fake fraud alert is similar to a phishing scam. The scammer will contact you by email or phone and tell you there is a problem with your account. To fix the problem or upgrade the security of your account, they will ask you to confirm all your personal details. Scammers have been known to make up all sorts of stories to trick their victims.

Some people are told that their credit card has been used to make a suspicious purchase in a foreign country and others have simply been told that their details are needed for a security and maintenance upgrade.

Banks and financial institutions will often contact people to alert them to suspicious activity on their account, but they will never ask you to provide your details online or over the phone. If in doubt, ring the bank yourself.

Card Skimming

Card skimming is the copying of information from the magnetic strip of a credit card or ATM card. Once scammers have skimmed your card, they can create a fake or ‘cloned’ card with your details to make charges on your account. Or they may simply photocopy your card and use the details.

Be suspicious if a shop assistant insists on taking your card out of your sight to process your transaction or tries to swipe your card through more than one machine. If the machine doesn’t look right to you, don’t use it.

Remember

- A legitimate bank or financial institution will never ask you to click on a link in an email or send your account details through an email or website.

- Never send your personal, credit card, or account information by email or enter it on a website that you are not certain is genuine.

- Don’t give out your personal, credit card, or account details over the phone unless you made the call and the phone number came from a trusted source.

Think

Are the contact details provided in an email correct? Telephone your bank or financial institution to ask whether the email you received from them is genuine. Use a phone number that you know is legitimate, from an account statement, the phone book, or the back of your ATM card—do not rely on the contact details provided in the email.

Ask Yourself

Are the contact details provided in an email correct? Telephone your bank or financial institution to ask whether the email you received from them is genuine. Use a phone number that you know is legitimate, from an account statement, the phone book, or the back of your ATM card—do not rely on the contact details provided in the email.